Turtle Talk - 24th December 2012

Don't look for supernormal gains

Jayant Pai | [email protected]

Investing can be fruitful if one approaches them as 'investments' rather than lotteries

Investing can be fruitful if one approaches them as 'investments' rather than lotteriesThe primary markets have been quite somnolent for the past three years or so. During this period, while institutions have been fairly active in the Qualified Institutional Placement (QIP) market, retail investors have largely been ignored. Now that a revival of the primary market appears to be on the cards, it may be a good time to revisit a few basic tenets of investing in this market.

The primary market largely comprises of two segments: 1. Initial Public Offerings (IPO) 2. Follow On Public Offerings

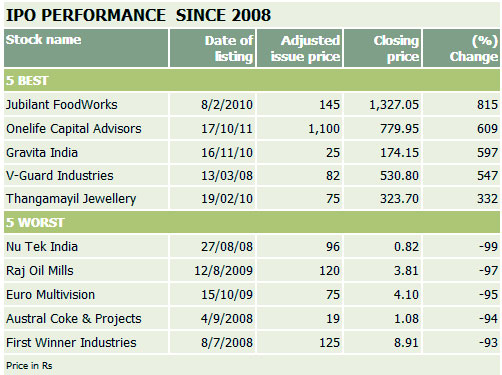

Worldwide, IPO markets are often viewed as a lottery, wherein successful allottees are able to sell their holdings at a huge premium on listing. This belief may still hold good in some countries, but in India this arbitrage has faded over time. This is due to:

Free pricing of IPOs: Today's newbies may find the old 'war-stories' of fabulous gains from IPOs very alluring. However, sadly for them, times have changed. Prior to 1992, IPOs were priced as per an ultra-conservative formula, which invariably resulted in allottees enjoying super-normal gains. However, since 1992, this formula has been dispensed with and promoters are free to price their IPOs as per market demand. Hence, a lot of value is appropriated by the promoter at the IPO stage itself. Since it is a zero-sum game, the promoter's gain is the allottee's loss (albeit notional). Hence, while it may happen once in a while, it is unrealistic to treat supernormal gains as "Par-For-The-Course".

The dice is loaded against you: Promoters have access to the best investment bankers. It is their job to please their client (in this case, the promoter) and ensure that they get the biggest bang for the buck. Obviously, this means that your interest as an investor is rarely, if ever, taken into account.

Despite these factors, investing in IPOs can be reasonably fruitful if one approaches them as 'investments' rather than lotteries. Conduct the requisite due diligence by:

Looking at valuations and not 'values': This may sound strange, but many retail investors actually make decisions based on the nominal value of the shares being offered, rather than the valuations. For instance, one of my friends preferred the Bharti Infratel issue to the CARE IPO as the former was priced at around Rs 230 while the latter was at Rs 750. I had to then explain to him the CARE issue was actually priced more reasonably based on the regular valuation metrics of Price/Earnings etc. Investors make this mistake in the secondary market too, when they prefer to purchase penny stocks merely because of low stock price.

In fact, many a times, IPOs which are made during bear markets turn out to be much better investments as the valuations are usually at sensible levels. Also, the chances of allotment are higher due to the general apathy in the market.

Undertaking peer comparisons: Today, it is rare to come across any IPO where peer comparisons are difficult to make (although Bharti Infratel was one such). Hence, an investor should always compare the company making the offer, with other listed peers. Only then will one know whether applying for the IPO is worthwhile or not.

If the new company is not markedly different from its peers, it may make sense to apply only if it is offering its shares at a reasonable valuation discount.

Investing in Follow-On Public Offerings (FPOs): This pertains to further equity issuances made by listed entities. Here, the decision whether to apply or not, is slightly easier, as comparisons between the FPO price and the current market price can be made on a continuous basis. Sometimes, poor market conditions may result in the offer price being higher than the market price, due to the time lag between the offer price being announced and the issue opening. In such cases, you could purchase the shares from the secondary market, rather than applying in the FPO, in case you are bullish about the company's prospects.

A few more general points pertaining to issuances:

- Do not purchase IPOs for the "Listing Pop". It is vital that one adopts a long-term view, based on the company's fundamentals, so that one is not saddled with a 'lemon' in case market conditions are adverse at the time of listing. In other words, purchase the business and not merely the stock at the time of the IPO.

- Avoid subscribing to IPOs 'On Margin': This involves you subscribing to the issue by only putting up a small percentage of the total sum, the balance amount being borrowed from "Margin Financiers". Such financiers have a lien on the equity shares that you apply for. In other words you are leveraging in order to apply for a larger quantity of shares. While it is wonderful if the price rises on listing, the converse could cause you severe financial strain as you would be bound to repay the loan irrespective of the fact that the stock may be trading below the offer price.

- Do not get swayed by the discount: Many companies offer a small discount to retail applicants at the time of the IPO. While this is good, it should not be the sole determinant while investing. A poor quality IPO's post-listing price may go far below this discounted offer price too.

- Do not think you are the smartest: Sometimes investors invest in 'hot' IPOs despite the company's fundamentals being suspect, merely because they 'are certain' that they can palm off their holdings at a huge premium post-listing. This is known as the 'Greater Fool Theory'. However, this tactic can backfire badly, as investors in Reliance Power, belatedly realised.

- Do not blindly trust the Government: If you believe that only private promoters are out to maximise their gains...think again. The Central Government has a chequered history with respect to the Offers For Sale (OFS) / IPOs/ FPOs conducted in the past. While investors have rejoiced in some cases (For instance, Maruti, Coal India and Oil India), they also have been bitterly disappointed in case of some others (For instance, IPCL and NHPC). Hence the principle of 'Caveat Emptor' applies to such issuances as well.

- Merely because an offering is vetted by SEBI, it should not be construed as SEBI vouching for the quality of the issue.

Today, it appears that we are in the first phase of a new bull market. Currently the IPO market is not very vibrant, but it is expected to get more bubbly in line with the secondary markets. This is a good time for investors to learn from the past so as to eschew grief in the future.

This article first appeared in Business Standard on December 16, 2012.

Floating Rate funds: From the WMG Desk

Ashish Shah | [email protected]

Floating rate funds are basically debt funds which invest in floating rate securities. So if the interest rates rise, the return on these underlying securities (such as corporate bonds, Govt. securities etc) rises and vice versa. In a floating rate instrument, the coupon rate is not fixed; rather it is benchmarked against a market-driven rate like the Mumbai Interbank Offered Rate (MIBOR), for instance. The coupon rate on a floating rate instrument is adjusted to the benchmark rate - let's say the MIBOR. So every time the MIBOR fluctuates, the coupon rate on the instrument is adjusted accordingly. That is why the coupon rate is referred to as 'floating rate'.

What is the advantage of Floating Rate fund?

Before explaining this, let's understand the relation between interest rate and returns of debt instruments. There is an inverse price-yield relationship of bonds. Bond prices fall when interest rates rise, and the prices rise when rates fall. This is not the same in case of fixed rate funds. A fund which invests in fixed rate securities faces a different risk. When the interest rates rise, these debt instruments with fixed rates fall in value and so does the mutual fund NAV. The longer the duration, the greater the impact on the principal amount or NAV of interest rate changes. Thus, rising interest rate will cause bond fund with duration of 10 years to fall more than that of a bond fund with an average duration of two years. As a result these fixed rate funds show a higher return in falling rate scenario and poor returns or even negative returns in an increasing rate scenario.

Example:

Suppose you buy a five-year corporate bond of Hindalco Ltd. that pays 1% more than the five-year Govt. Security yield, and the benchmark is reset every six months; a reset means that the five-year G-Sec yield will be reviewed every six months. Suppose the five-year G-Sec yield on January 1, 2010 is 7.5 per cent, Hindalco Ltd. will pay an interest of 8.50% on its bond. If the G-Sec yield increases to 8% on June 1, 2010, the reset date, Hindalco Ltd. bond will pay 9%. You will note that the bond's yields are linked to the current market rate. If the market rate rises, the bond's yield will also rise on the reset date. This is not the case with fixed income bonds, which is why their prices fall to adjust to the market rate. As the floating rate bond adjusts to the market price, its price will not fall as much as the fixed income bond's. The fall in floating rate bond will depend on the period of reset. The lesser the gap between the resets, the lower will be the fall in price. This is because the bond will start earning the market rate in shorter time. Thus, by investing in floating rate instruments, Floating rate fund seeks to reduce the fall in bond prices due to rise in interest rates.

Volatility of equity markets is something that is widely accepted by investors as an investment hazard. However, on the debt side, investors haven't got used to dealing with interest rate volatility. Volatility in debt funds has come as a rude shock to most risk-averse investors and runs contrary to their view on debt funds, which is one of stability and consistency. Floating rate funds strive to fulfill their role as a stabilising force in debt portfolios. The floating rate fund is ideally suitable for people who want a stable rate of return without any volatility. A floating rate income fund has become something of a necessity with a definite role to play in the future in view of increasing volatility in debt markets. Investors need to understand this and make adjustments in their overall asset allocation.